Last reviewed: May 2026 | All regulatory references reflect current DGT / BKPM / BPJS frameworks.Reviewed: JCSS Team

| Obligation | Frequency | Standard Deadline | Authority | System |

|---|---|---|---|---|

| VAT Return (SPT Masa PPN) | Monthly | 30th of following month | DGT | CoreTax / e-Faktur |

| PPh 21 Withholding Report | Monthly | 20th of following month | DGT | CoreTax |

| PPh 23/26 Withholding Report | Monthly | 20th of following month | DGT | CoreTax |

| BPJS Ketenagakerjaan | Monthly | 15th of following month | BPJS-TK | SIPP Online |

| BPJS Kesehatan | Monthly | 10th of following month | BPJS-K | Edabu |

| LKPM Investment Report | Quarterly | End of following month | BKPM / OSS | OSS Portal |

| Corporate Income Tax (PPh Badan) | Annual | 4 months after fiscal year-end | DGT | CoreTax |

| Annual SPT Badan Filing | Annual | 4 months after fiscal year-end | DGT | CoreTax |

| Transfer Pricing Documentation | Annual | By SPT filing date | DGT | CoreTax |

| Statutory Financial Audit | Annual | Varies by threshold | MoLHR / DGT | — |

Direct Answer: A foreign-owned PT PMA carries five core monthly compliance streams that must be executed in sequence and filed through Indonesia's CoreTax system (Sistem Inti Administrasi Perpajakan — SIAP), which became the unified filing platform effective January 2025.

| # | Obligation | Legal Basis | Filing System | Deadline |

|---|---|---|---|---|

| 1 | VAT invoicing & SPT Masa PPN | Law No. 42/2009; PMK-18/2021 | CoreTax / e-Faktur | 30th of following month |

| 2 | PPh 21 — Employee income tax withholding | Law No. 36/2008; PMK-168/2023 | CoreTax | 20th of following month |

| 3 | PPh 26 — Foreign employee withholding | Law No. 36/2008 Art. 26 | CoreTax | 20th of following month |

| 4 | PPh 23 — Service / royalty withholding | Law No. 36/2008 Art. 23 | CoreTax | 20th of following month |

| 5 | BPJS Ketenagakerjaan contributions | Law No. 24/2011; PP No. 44/2015 | SIPP Online | 15th of following month |

| 6 | BPJS Kesehatan contributions | Law No. 40/2004; Perpres No. 64/2020 | Edabu Portal | 10th of following month |

| Source | URL |

|---|---|

| Directorate General of Taxes (DGT / DJP) — Official Portal | pajak.go.id |

| CoreTax System Portal | coretax.pajak.go.id |

| PMK-168/2023 (PPh 21 TER Rules) | jdih.kemenkeu.go.id |

| BPJS Ketenagakerjaan — SIPP Online | sipp.bpjsketenagakerjaan.go.id |

| BPJS Kesehatan — Edabu | edabu.bpjs-kesehatan.go.id |

Practitioner Note: The shift from the old e-SPT desktop application to CoreTax means that all data entry, validation, and submission now occurs in a browser-based environment. Companies that have not migrated their eFIN credentials and user access to CoreTax by their first 2025 filing date face immediate filing-failure risk.

Direct Answer: CoreTax (officially: Sistem Inti Administrasi Perpajakan / SIAP) replaces multiple legacy DGT systems — including e-SPT, e-Faktur desktop client, DJP Online, and e-Filing — with a single integrated cloud-based platform. For PT PMAs, the practical operational changes are significant.

| Process | Pre-CoreTax (Legacy) | Post-CoreTax (2025+) |

|---|---|---|

| Tax invoice creation | e-Faktur desktop application (installed locally) | Browser-based within CoreTax portal |

| VAT return preparation | e-SPT PPN (desktop) → upload | Direct input/API into CoreTax |

| Tax payment | Manual SSP → bank teller or ATM | e-Billing generated inside CoreTax; paid via virtual account |

| e-FIN management | Per-company e-FIN | Integrated user authentication (SSO) |

| Invoice numbering | NSFP batch allocation from DGT | Sequential system-generated within CoreTax |

| Data validation | Post-submission by DGT | Real-time pre-submission validation rules |

| Audit trail | Local desktop backups | Server-side CoreTax audit log |

| Source | URL |

|---|---|

| CoreTax Official Portal | coretax.pajak.go.id |

| DGT CoreTax Information Hub | pajak.go.id/unit/coretax |

| PER-06/PJ/2024 (CoreTax Technical Regulation) | pajak.go.id |

| PMK-18/2021 (e-Faktur and VAT Invoicing Rules) | jdih.kemenkeu.go.id |

Direct Answer: Indonesia's monthly tax deadlines follow a structured calendar established under the General Tax Provisions Law (KUP Law — Law No. 28/2007 as amended) and related Ministry of Finance regulations. Missing these deadlines triggers automatic administrative penalties.

| Tax Type | Legal Basis | Payment Deadline | Filing (SPT) Deadline | Late Payment Penalty | Late Filing Penalty |

|---|---|---|---|---|---|

| VAT (PPN) | UU 42/2009; PMK-18/2021 | End of following month | End of following month | 2.5% p.m. of underpayment (KMK-541/KMK.04/2000 rate; now reference rate + 5%) | IDR 500,000 per return |

| PPh 21 (employees) | UU 36/2008; PMK-168/2023 | 10th of following month | 20th of following month | Reference rate + 5% p.a. pro-rated | IDR 100,000 per return |

| PPh 23 (domestic services) | UU 36/2008 Art. 23 | 10th of following month | 20th of following month | Reference rate + 5% p.a. pro-rated | IDR 100,000 per return |

| PPh 26 (foreign parties) | UU 36/2008 Art. 26 | 10th of following month | 20th of following month | Reference rate + 5% p.a. pro-rated | IDR 100,000 per return |

| PPh 4(2) (final tax) | UU 36/2008 Art. 4(2) | 10th of following month | 20th of following month | Reference rate + 5% p.a. pro-rated | IDR 100,000 per return |

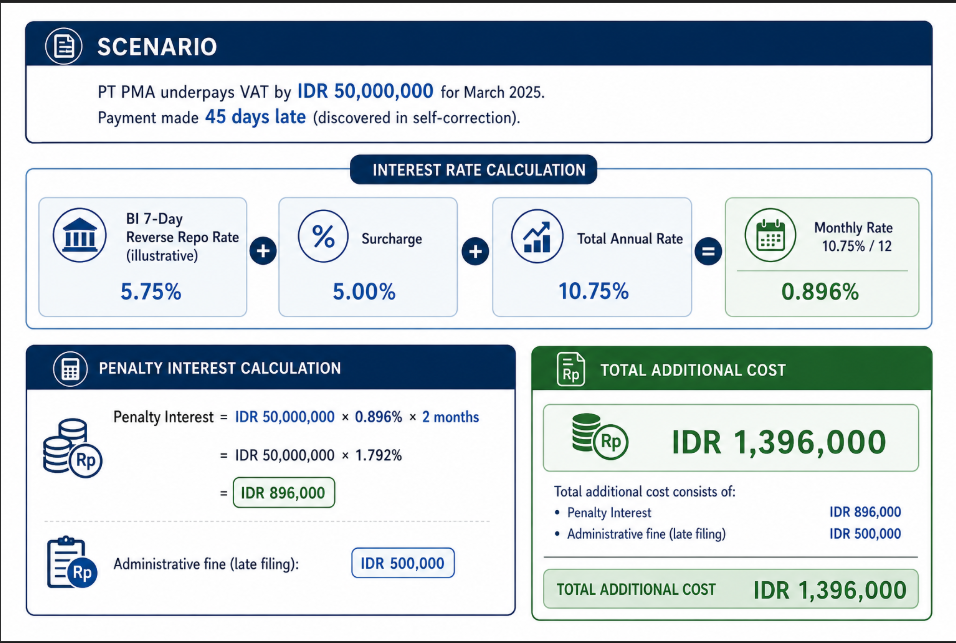

Reference Interest Rate: Under the Omnibus Law amendments (HPP Law — Law No. 7/2021), the penalty interest rate is calculated using Bank Indonesia's benchmark rate plus a surcharge, announced monthly by the Ministry of Finance. Check the current rate at jdih.kemenkeu.go.id.

If a deadline falls on a public holiday or weekend, it automatically shifts to the next working business day. Indonesia has a significant number of national public holidays (typically 16–18 per year); PT PMAs should maintain an adjusted compliance calendar annually.

| Source | URL |

|---|---|

| DGT — Tax Deadlines Reference | pajak.go.id |

| HPP Law (Law No. 7/2021) — KUP Amendments | jdih.kemenkeu.go.id |

| PMK-9/2018 (Late Payment & Filing Procedures) | jdih.kemenkeu.go.id |

| Bank Indonesia — Benchmark Rate | bi.go.id |

Direct Answer: Indonesia's tax law requires companies to maintain complete, accurate, and accessible records that support every line of every tax return filed. Under the KUP Law (Article 28–29), records must be retained for 10 years and must be produced on demand during a DGT audit.

| Document Category | Specific Documents | Retention Period | Format |

|---|---|---|---|

| VAT — Sales | e-Faktur (tax invoice) files, sales contracts, delivery orders, bank receipts | 10 years | Electronic (CoreTax) + physical backup |

| VAT — Purchases | Incoming e-Faktur, purchase orders, goods receipt notes, import customs declarations (PIB) | 10 years | Electronic + physical |

| PPh 21 / Payroll | Monthly payroll register, employment contracts, PTKP declarations (Form 1721-A1), TER calculation worksheets | 10 years | Electronic + physical |

| PPh 23/26 | Service agreements, invoices from vendors, withholding slips (Bukti Potong), DTA relief applications (Form DGT-1/DGT-2) | 10 years | Electronic + physical |

| BPJS | Monthly BPJS billing statements, payment receipts, employee participation certificates | 5 years minimum | Electronic + physical |

| Bank Records | Bank statements, transfer confirmations for tax payments, e-Billing payment confirmations | 10 years | Electronic + physical |

| General Ledger | Chart of accounts, journal entries, trial balance, reconciliations | 10 years | Electronic (ERP) + physical |

CoreTax imposes real-time data integrity rules. An e-Faktur that fails validation (e.g., mismatched NPWP, incorrect tax base, wrong invoice date format) is rejected immediately — meaning a rejected invoice creates a VAT input tax credit gap for the buyer and a reporting gap for the seller.

Best practice checklist for monthly document management:

| Source | URL |

|---|---|

| KUP Law Art. 28–29 (Record-Keeping Obligations) | jdih.kemenkeu.go.id |

| PER-17/PJ/2015 (Bookkeeping Requirements for Taxpayers) | pajak.go.id |

| PMK-18/2021 (VAT Invoice Rules) | jdih.kemenkeu.go.id |

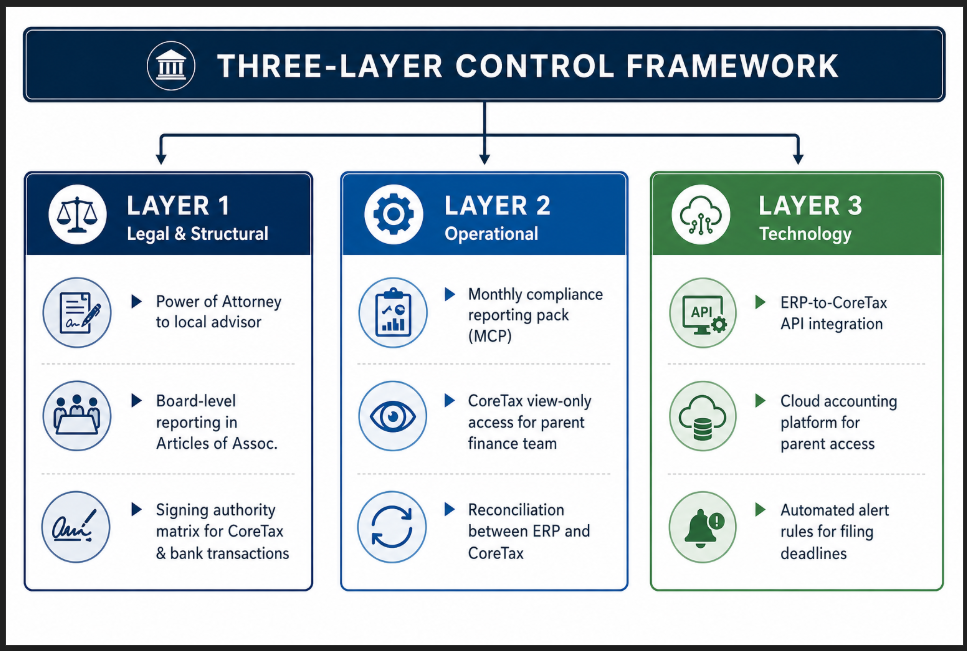

Direct Answer: Remote oversight of an Indonesian PT PMA's tax compliance requires a structured three-layer monitoring framework combining legal, operational, and technological controls. The parent company cannot assume that local management alone will flag issues in time to prevent penalties.

| Report | Description | Prepared By |

|---|---|---|

| VAT Position Summary | Output vs. input VAT, net payable/refundable, SPT filing confirmation | Local accountant |

| PPh 21 Payroll Summary | Headcount, gross payroll, TER-based withholding, BPJS contributions | Local HR/Payroll |

| WHT Register (PPh 23/26) | All service payments subject to withholding, Bukti Potong issued | Local accountant |

| Bank Reconciliation | Confirms all tax payments cleared, matches CoreTax e-Billing receipts | Local accountant |

| BPJS Payment Confirmation | Screenshots/receipts of BPJS-TK and BPJS-K payments | Local HR |

| Exceptions & Risk Log | Any late filings, penalties incurred, DGT correspondence received | Local advisor |

| Next-Month Deadline Calendar | Adjusted for public holidays | Local advisor |

| Parent Location | Time Difference (WIB — UTC+7) | Recommended Reporting Window |

|---|---|---|

| Singapore (SGT, UTC+8) | +1 hour | End of week — minimal friction |

| India (IST, UTC+5:30) | −1.5 hours | Morning IST = late morning WIB |

| USA East Coast (EST, UTC−5) | −12 hours | WIB afternoon = EST morning |

| USA West Coast (PST, UTC−8) | −15 hours | WIB afternoon = PST early morning |

| Source | URL |

|---|---|

| DGT CoreTax — User Access Management | coretax.pajak.go.id |

| BKPM — LKPM Reporting Portal (Investment Monitoring) | oss.go.id |

| Ministry of Investment — PT PMA Obligations | investindonesia.go.id |

Direct Answer: Indonesia's penalty regime for late and inaccurate tax filings is multi-layered — combining administrative fines, interest surcharges, and in serious cases, criminal sanctions. The regime was restructured under the HPP Law (Law No. 7/2021), which replaced fixed statutory interest rates with a market-linked formula.

| Violation | Legal Basis | Penalty |

|---|---|---|

| Late VAT return filing | KUP Art. 7 | IDR 500,000 per late return |

| Late PPh 21/23/26 return filing | KUP Art. 7 | IDR 100,000 per late return |

| Late tax payment (underpayment) | KUP Art. 9(2a) | BI rate + 5% p.a., pro-rated monthly, max 24 months |

| Incorrect return — voluntary correction | KUP Art. 8 | BI rate + 5% p.a. on underpayment |

| Incorrect return — DGT-initiated correction (SKPKB) | KUP Art. 13 | 75% surcharge on tax underpayment (administrative) |

| Failure to keep required records | KUP Art. 39 | Criminal: 6 months–6 years imprisonment + fine 2–4x tax |

| Intentional tax evasion | KUP Art. 39 | Criminal: 6 months–6 years + fine 2–4x tax underpaid |

| Incorrect e-Faktur (VAT invoice) | PER-03/PJ/2022 | Input VAT credit disallowed for recipient; issuer subject to audit |

Important: The multiplier used in SKPKB assessments (DGT-initiated corrections after audit) is 75% of the tax underpayment — not a percentage-per-month calculation. For a IDR 500,000,000 underpayment, this equals IDR 375,000,000 in surcharges alone, before interest.

| Source | URL |

|---|---|

| KUP Law (Law No. 28/2007 as amended by HPP Law No. 7/2021) | jdih.kemenkeu.go.id |

| HPP Law — Penalty Rate Reform | jdih.kemenkeu.go.id |

| Bank Indonesia — Current Benchmark Rate | bi.go.id |

| DGT — Penalty and Interest Explainer | pajak.go.id |

Direct Answer: The Dinas Tenaga Kerja (Disnaker) — Indonesia's regional labor offices — operate a parallel compliance stream to the DGT's tax system. For a PT PMA, these systems are interdependent: payroll data feeds into both BPJS contributions and PPh 21 withholding, and inconsistencies between the two create audit exposure in both regulatory domains.

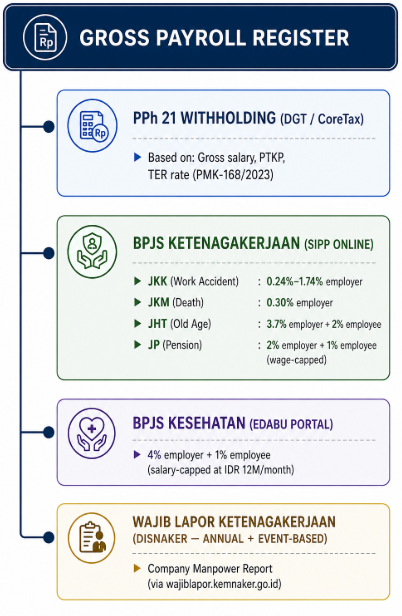

| Program | Employer Contribution | Employee Contribution | Wage Cap |

|---|---|---|---|

| JKK (Work Accident) | 0.24%–1.74% (risk-based) | — | No cap |

| JKM (Death Insurance) | 0.30% | — | No cap |

| JHT (Old Age Savings) | 3.7% | 2% | No cap |

| JP (Pension) | 2% | 1% | IDR 9,559,600/month (2024 rate; reviewed annually) |

| BPJS Kesehatan | 4% | 1% | IDR 12,000,000/month |

| Report | Frequency | Platform | Legal Basis |

|---|---|---|---|

| Wajib Lapor Ketenagakerjaan (Manpower Registration) | Annual + any workforce change | wajiblapor.kemnaker.go.id | Law No. 7/1981 |

| Employment of Foreign Workers (RPTKA) | Per foreign hire event | Sisnaker | PP No. 34/2021 |

| Company Regulations (Peraturan Perusahaan) | Every 2 years (>10 employees) | Disnaker | Law No. 13/2003 |

| Source | URL |

|---|---|

| Ministry of Manpower — Sisnaker Portal | kemnaker.go.id |

| Wajib Lapor Ketenagakerjaan Portal | wajiblapor.kemnaker.go.id |

| BPJS Ketenagakerjaan — Official Portal | bpjsketenagakerjaan.go.id |

| BPJS Kesehatan — Official Portal | bpjs-kesehatan.go.id |

| PP No. 44/2015 (BPJS-TK Contribution Rates) | jdih.kemenkeu.go.id |

| Perpres No. 64/2020 (BPJS Kesehatan Contribution Rates) | jdih.setneg.go.id |

Direct Answer: Yes — and for most small to mid-sized PT PMAs, outsourcing monthly compliance to a qualified local accounting and tax advisory firm is the operationally superior choice. Indonesian tax compliance has become increasingly technical with the CoreTax migration, the PPh 21 TER reform (PMK-168/2023), and real-time e-Faktur validation requirements.

| Function | Can Be Outsourced | Cannot Be Outsourced |

|---|---|---|

| Monthly bookkeeping and GL maintenance | ✅ Yes | — |

| VAT invoice preparation (e-Faktur) | ✅ Yes | Director's legal responsibility for accuracy |

| SPT Masa PPN preparation and filing | ✅ Yes | Final approval remains with company |

| PPh 21 payroll calculation (TER) | ✅ Yes | — |

| BPJS contribution calculation and payment | ✅ Yes | — |

| CoreTax submission | ✅ Yes (via PoA or authorized user) | — |

| Tax audit representation | ✅ Yes (tax consultant with STTD license) | — |

| Signing of tax returns | ❌ No | Must be signed by company director or authorized proxy with PoA |

| Business decisions on tax planning | ❌ No | Management responsibility |

A well-structured outsourcing arrangement should include:

| Source | URL |

|---|---|

| DGT — Registered Tax Consultant Verification | pajak.go.id |

| IKPI (Indonesian Tax Consultant Association) | ikpi.or.id |

| PMK-111/2014 (Tax Consultant Licensing) | jdih.kemenkeu.go.id |

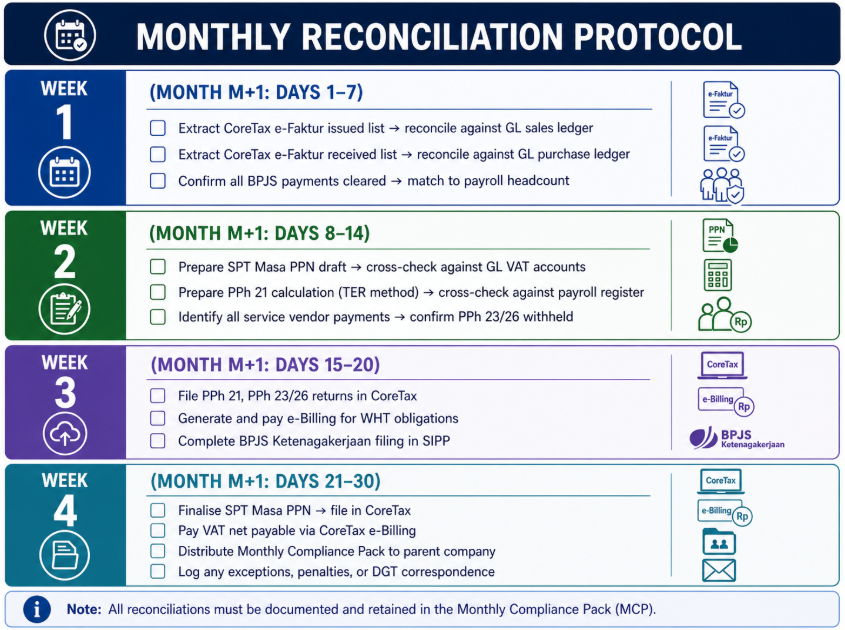

Direct Answer: Failure to reconcile ERP/accounting records against CoreTax data monthly is one of the highest-risk compliance gaps for PT PMAs. The CoreTax system maintains an independent, government-held record of all transactions — and discrepancies between the government's data and the company's books are a primary trigger for DGT audit selection.

| Discrepancy Type | Root Cause | DGT Consequence | Financial Exposure |

|---|---|---|---|

| Sales in GL exceed VAT returns | Unissued e-Faktur on some transactions | SKPKB for underpaid VAT + 75% surcharge | High |

| Input VAT claimed without matching e-Faktur | Vendor-side e-Faktur cancellation undetected | Input VAT credit disallowed | Medium-High |

| PPh 21 withheld ≠ payroll register | Mid-month salary adjustments not reflected in CoreTax | WHT underpayment assessment | Medium |

| PPh 23 not withheld on service payments | Vendor invoices booked but WHT obligations missed | Assessment on gross payment amount | High |

| BPJS contributions don't match payroll headcount | New hires registered late in SIPP | Disnaker and BPJS audit; retroactive contributions | Medium |

| Bank payments don't match CoreTax e-Billing | Payments made without generating e-Billing first | Payment not credited by DGT; appears as non-payment | High |

| Source | URL |

|---|---|

| DGT — Audit Selection Criteria (Public Information) | pajak.go.id |

| CoreTax Data Reconciliation Guide | coretax.pajak.go.id |

| PER-07/PJ/2017 (Tax Audit Procedures) | pajak.go.id |

Direct Answer: Month-to-month spikes in VAT, WHT, or payroll tax figures are a significant audit trigger in CoreTax's automated risk-scoring model. DGT's system applies pattern-recognition analytics to all taxpayer data — sudden large variances prompt automated review flags and, in some cases, direct audit selection.

| Spike Type | Common Cause | Prevention Control |

|---|---|---|

| VAT output spike | Large one-time sale or project milestone billing | Pre-flag large invoices; ensure e-Faktur issued in same period as delivery |

| VAT input spike | Batch processing of vendor invoices from prior months | Implement same-month invoice booking policy; maximum 3-month posting window |

| PPh 21 spike | Annual bonus payments, mid-year salary restructuring | Model bonus impact on TER rate in advance; notify CoreTax preparer |

| PPh 23 spike | Large one-time service contract payment | Confirm WHT rate and treaty applicability before payment processing |

| Payroll headcount spike | Bulk new hires not reflected in prior month BPJS | Weekly BPJS registration updates; not end-of-month batch processing |

| Intercompany transaction spike | Management fees, royalties, or loans booked irregularly | Establish intercompany billing on fixed monthly schedule |

1. Cut-Off Date Discipline Establish a hard monthly cut-off date (e.g., the 25th of each month) after which no transactions are booked to the closing period without senior approval. This prevents last-minute entries that distort period comparisons.

2. Intercompany Transaction Calendar If your PT PMA receives management fees, royalties, IT service charges, or loan interest from related overseas entities, these should be billed on a fixed monthly schedule — not quarterly or on-demand — to prevent large quarterly WHT spikes.

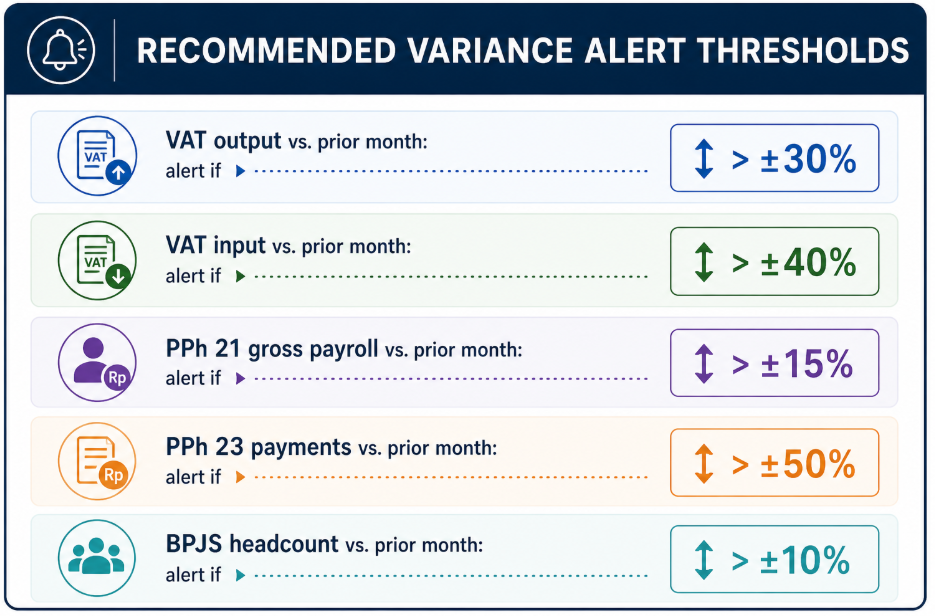

3. Variance Threshold Alerts Set automated variance alerts in your accounting system:

4. Narrative Documentation for Legitimate Spikes Where a spike is commercially justified (e.g., a major project completion triggering a large invoice), prepare a brief variance explanation memo that is retained on file. If DGT raises a query, this memo supports the taxpayer's position without requiring an emergency audit response.

| Source | URL |

|---|---|

| DGT — Risk-Based Compliance Program | pajak.go.id |

| CoreTax Taxpayer Compliance Portal | coretax.pajak.go.id |

| SE-05/PJ/2022 (DGT Compliance Risk Management) | pajak.go.id |

Direct Answer: A foreign-owned PT PMA faces seven core annual compliance obligations that collectively integrate tax reporting, investment monitoring, corporate governance, and transfer pricing documentation. These obligations have become increasingly interconnected following Indonesia's adoption of OECD BEPS Action Plan recommendations and the rollout of CoreTax Phase II (effective 2025–2026).

| # | Obligation | Legal Basis | Filing Authority | Deadline (Calendar-Year) |

|---|---|---|---|---|

| 1 | Annual Corporate Income Tax Return (SPT Tahunan PPh Badan) | UU 36/2008 (Income Tax Law); HPP Law 7/2021 | DGT | 30 April |

| 2 | Audited Financial Statements (if required) | Law 40/2007 (Limited Liability Companies); PMK-8/2021 | MoLHR; DGT; OJK (if applicable) | Audit completion: 31 Jan; Filing: with SPT |

| 3 | Transfer Pricing Documentation (TP Doc) | PMK-213/2016; PER-22/PJ/2013; OECD Guidelines | DGT | 30 April (with SPT) or 1 month after audit request |

| 4 | Country-by-Country Report (CbCR) | PMK-213/2016; PER-29/PJ/2017 | DGT | 31 July (12 months after fiscal year-end) |

| 5 | LKPM Annual Investment Activity Report | Law 25/2007 (Investment); PP 5/2021 | BKPM / OSS | End of February (following year) |

| 6 | Annual General Meeting of Shareholders (RUPS) | Law 40/2007 Art. 78–79 | Internal (documented); MoLHR (report) | Within 6 months of FYE |

| 7 | Annual Manpower Compliance Report (Wajib Lapor) | Law 13/2003; Permenaker 16/2023 | Disnaker | 31 May |

The SPT Tahunan is the capstone document of Indonesia's tax compliance year. It consolidates:

Key 2026 Update: CoreTax Phase II now requires XBRL-tagged financial statements for all PT PMAs with annual revenue exceeding IDR 50 billion. This means financial data must be submitted in a machine-readable format that auto-populates tax reconciliation fields and allows real-time DGT validation.

Audit Requirement Thresholds (PMK-8/2021):

A PT PMA must engage an independent public accountant (Kantor Akuntan Publik / KAP) to audit its annual financial statements if it meets any one of the following criteria:

| Criterion | Threshold |

|---|---|

| Total assets | ≥ IDR 50 billion |

| Annual revenue | ≥ IDR 50 billion |

| Public interest entity | Banking, insurance, capital markets, state-owned enterprises, pension funds |

| Shareholder requirement | Foreign shareholders holding ≥ 20% may require audit by agreement |

Audit Standards: Audits must be conducted in accordance with Indonesian Financial Accounting Standards (SAK) — specifically PSAK (Pernyataan Standar Akuntansi Keuangan), which has been substantially converged with IFRS as of 2024.

Key 2026 Update: PSAK 74 (Revenue from Contracts with Customers — equivalent to IFRS 15) and PSAK 71 (Financial Instruments — equivalent to IFRS 9) are now mandatory for all PT PMAs. Revenue recognition timing and financial asset classification must align with these standards before tax reconciliation.

Who Must Prepare TP Doc? Any PT PMA that engages in related-party transactions with:

TP Doc Components (Three-Tier Structure per OECD BEPS Action 13):

Submission Timing:

CbCR Filing Requirement: PT PMAs that are part of a multinational enterprise (MNE) group with consolidated group revenue ≥ EUR 750 million must file CbCR in Indonesia if the parent entity is:

CbCR Contents:

Deadline: 31 July (12 months after the end of the fiscal year of the ultimate parent entity)

What is LKPM? LKPM (Laporan Kegiatan Penanaman Modal) is Indonesia's investment realization tracking system managed by BKPM (now integrated into the Ministry of Investment). It serves as the government's primary tool for monitoring whether PT PMAs are meeting their stated investment plans.

LKPM Quarterly vs. Annual:

Key Data Points in LKPM Annual:

| Data Category | What DGT Cross-Checks |

|---|---|

| Investment realization (capital deployed) | Fixed asset additions in financial statements |

| Employment (Indonesian vs. foreign workers) | PPh 21 annual payroll summary; BPJS headcount |

| Production/revenue | Revenue figure in SPT Tahunan |

| Export activity | Customs data (if applicable) |

| Domestic content compliance | For certain sectors with local content requirements |

2026 Update: LKPM is now auto-linked to CoreTax data. Discrepancies between LKPM-reported revenue and SPT Tahunan-reported revenue trigger automated review flags.

Legal Requirement: Under Law 40/2007 (Limited Liability Companies), every PT PMA must hold an Annual General Meeting of Shareholders (RUPS Tahunan) within 6 months of the end of the fiscal year.

RUPS Agenda Must Include:

Documentation Required:

Filing Obligation: While RUPS itself is an internal corporate governance event, certain outcomes (e.g., director changes, dividend distribution) must be reported to the Ministry of Law and Human Rights (Kemenkumham) via the AHU Online system.

What is Wajib Lapor? The annual manpower report filed via Sisnaker (Sistem Informasi Ketenagakerjaan) provides the Ministry of Manpower (Kemnaker) and local Disnaker offices with:

Deadline: 31 May (following the reporting year)

Cross-Linkage with Tax Compliance:

| Source | URL |

|---|---|

| DGT — Annual SPT Tahunan Filing Portal (CoreTax) | coretax.pajak.go.id |

| Ministry of Finance Legal Database (PMK, KMK) | jdih.kemenkeu.go.id |

| PMK-8/2021 (Financial Statement Audit Thresholds) | jdih.kemenkeu.go.id |

| PMK-213/2016 (Transfer Pricing Documentation) | jdih.kemenkeu.go.id |

| PER-29/PJ/2017 (Country-by-Country Reporting) | pajak.go.id |

| OSS Portal — LKPM Filing | oss.go.id |

| Ministry of Law and Human Rights — AHU Online | ahu.go.id |

| Sisnaker Portal — Manpower Reporting | sisnaker.kemnaker.go.id |

| OECD — BEPS Action 13 Guidance | oecd.org/tax/beps |

Direct Answer: The annual SPT Tahunan PPh Badan (Corporate Income Tax Return) is fundamentally different in scope, complexity, and regulatory function from monthly tax returns (SPT Masa). Where monthly filings are transactional snapshots of withholding and VAT activity, the annual return is a comprehensive reconciliation of an entire fiscal year's financial performance against Indonesia's tax code.

| Dimension | Monthly SPT (Masa) | Annual SPT (Tahunan) |

|---|---|---|

| Scope | Single tax type, single month | All income, all deductions, full fiscal year |

| Tax Types Covered | PPh 21, PPh 23, PPh 26, PPN — separately | Consolidated PPh Badan (Corporate Income Tax) |

| Data Source | Transaction-level (invoices, payroll) | Financial statements + tax adjustments |

| Reconciliation Required | Against GL sub-ledgers | Against audited financials + commercial vs. fiscal book differences |

| Supporting Docs | E-faktur, Bukti Potong, payroll register | Full financial statements, TP Doc, audit report, tax ledger |

| Preparer Role | Accounting/tax staff | Tax manager + external auditor + tax consultant |

| Signing Authority | Authorized tax preparer or director | Must be signed by company director (or PoA holder) |

| Validation Logic | CoreTax real-time validation (format, NPWP) | XBRL taxonomy validation + cross-filed data checks |

| Amendment Process | Pembetulan (correction SPT) — relatively simple | Pembetulan SPT Tahunan — triggers full DGT review |

| Audit Trigger Weight | Low (unless repeated late filing) | High — annual SPT is primary audit selection input |

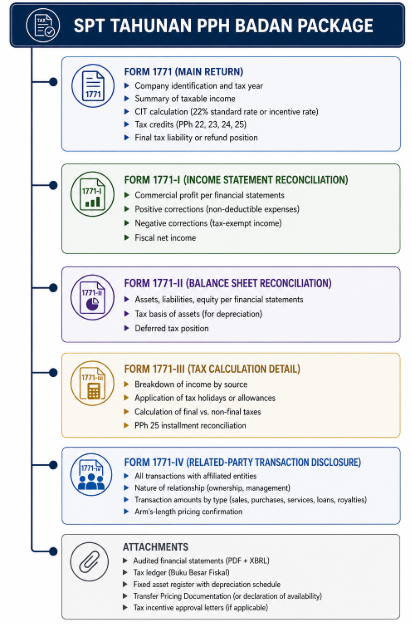

The annual CIT return consists of five main components filed through CoreTax:

One of the most technically demanding aspects of the annual SPT is the fiscal correction schedule. Indonesia's tax law does not recognize all expenses and income in the same manner as financial accounting standards (PSAK/IFRS).

Common Positive Corrections (Add Back to Taxable Income):

| Item | Commercial Treatment | Tax Treatment | Correction |

|---|---|---|---|

| Entertainment expenses exceeding deductibility limit | Expensed | 50% non-deductible | Add back 50% |

| Provisions (allowances) not yet realized | Expensed | Non-deductible until realized | Add back full amount |

| Donations to non-approved entities | Expensed | Non-deductible | Add back full amount |

| Non-business related expenses | Expensed | Non-deductible | Add back full amount |

| Depreciation (commercial) exceeding tax depreciation | Higher depreciation | Use tax rate and method | Add back excess |

| Fines and penalties | Expensed | Non-deductible | Add back full amount |

| Tax expense itself | Expensed | Non-deductible | Add back full amount |

Common Negative Corrections (Reduce Taxable Income):

| Item | Commercial Treatment | Tax Treatment | Correction |

|---|---|---|---|

| Dividend from domestic investments (DPP exemption) | Income | Exempt under Art. 4(3)(f) | Deduct full amount |

| Interest income subject to final tax (PPh 4(2)) | Income | Already taxed final | Deduct full amount |

| Tax depreciation exceeding commercial depreciation | Lower depreciation | Use tax rate | Deduct excess |

Throughout the year, PT PMAs make monthly installment payments (PPh 25) based on either:

The annual SPT reconciles these installments against the actual final tax liability:

| Step | Description | Calculation |

|---|---|---|

| 1 | Fiscal Net Income (after corrections) | Base amount |

| 2 | Apply CIT Rate | × 22% (standard rate or reduced rate if applicable) |

| 3 | Gross CIT Liability | Result after tax rate applied |

| 4 | Less: PPh 22 | Import withholding credit |

| 5 | Less: PPh 23 | Domestic withholding received |

| 6 | Less: PPh 24 | Foreign tax credit (if DTA applies) |

| 7 | Less: PPh 25 | Monthly installments paid |

| 8 | Net Tax Payable / (Overpayment) | Final position after all credits |

If Net Tax Payable > 0: Payment due by 30 April If Overpayment: Taxpayer can either:

What is XBRL? XBRL (eXtensible Business Reporting Language) is a machine-readable data standard that allows DGT's systems to automatically validate, analyze, and cross-check financial data without manual review.

Who Must Submit XBRL?

How XBRL Impacts Filing:

Practical Tip: Most major accounting software (SAP, Oracle, Accurate) now includes XBRL export functionality. Smaller PT PMAs typically engage their KAP (audit firm) to handle XBRL tagging.

| Source | URL |

|---|---|

| Income Tax Law (UU 36/2008 as amended) | jdih.kemenkeu.go.id |

| HPP Law (UU 7/2021) — CIT Rate Reduction to 22% | jdih.kemenkeu.go.id |

| PER-34/PJ/2017 (SPT Tahunan Filing Procedures) | pajak.go.id |

| SE-21/PJ/2023 (XBRL Taxonomy for Tax Reporting) | pajak.go.id |

| DGT — SPT Tahunan PPh Badan Guide | pajak.go.id |

| CoreTax XBRL Validation Tool | coretax.pajak.go.id |

Direct Answer: Annual tax and financial reporting deadlines are tiered and interdependent — the audit must be completed before the SPT can be filed, and the SPT deadline itself is non-negotiable and non-extendable except in extraordinary circumstances (natural disasters, systemic banking failures).

| Date | Milestone | Responsible Party | Consequence of Missing |

|---|---|---|---|

| 31 December | Fiscal year-end; accounts close | Finance team | N/A |

| 15 January | Year-end GL reconciliation complete; trial balance finalized | Finance team | Delays audit commencement |

| 31 January | External audit fieldwork complete; draft audit report | KAP (audit firm) | Cannot finalize SPT |

| 28 February | Audited financials approved by Directors; signed audit report | Board of Directors + KAP | SPT filing at risk |

| 15 March | Tax reconciliation (fiscal corrections) complete | Tax consultant / internal tax team | SPT filing rushed; errors likely |

| 25 March | Transfer Pricing Documentation finalized | TP consultant / tax team | TP Doc not available for DGT review |

| 30 March | Draft SPT Tahunan prepared and reviewed | Tax consultant + Finance Director | No time for error correction |

| 5 April | Final SPT Tahunan review and director signature | Company Director | Risk of late filing |

| 30 April | SPT Tahunan filed via CoreTax (HARD DEADLINE) | Tax preparer (authorized user) | Automatic IDR 1,000,000 penalty + interest on unpaid tax |

| 30 April | Payment of net tax liability (if payable) | Finance team | Late payment interest begins accruing immediately |

Short answer:No automatic extensions exist for SPT Tahunan filing in Indonesia.

Exception pathway: Under extraordinary circumstances (force majeure), a taxpayer can submit a written request to the local Tax Office (KPP) for a filing extension. The request must be submitted before the original deadline and must include:

Approval is rare and discretionary. Most requests are denied.

Practical alternative: Many PT PMAs file a preliminary SPT Tahunan (using unaudited financials or provisional tax calculations) by the deadline, then file a Pembetulan (correction return) within 2 years once final audited figures are available. This avoids the late filing penalty while preserving accuracy.

Warning: Filing a preliminary SPT and then correcting it later may increase audit scrutiny, as DGT systems flag frequent amendments as a risk indicator.

Indonesia's Default: Calendar year (1 January – 31 December)

Alternative Fiscal Year: PT PMAs can request approval to use a non-calendar fiscal year (e.g., 1 April – 31 March to align with parent company reporting) by submitting a formal application to the DGT before beginning operations.

Deadline Adjustment for Fiscal-Year Entities:

| Item | Deadline |

|---|---|

| Fiscal Year End | 31 March 2026 |

| Audit Completion | 31 July 2026 |

| LKPM Filing | 31 May 2026 |

| SPT Tahunan Filing (4 months after FYE) | 31 July 2026 |

| Tax Payment | 31 July 2026 |

Automatic Penalties (No Warning Issued):

| Penalty Type | Amount | Legal Basis |

|---|---|---|

| Late filing (SPT not submitted) | IDR 1,000,000 | KUP Law Art. 7 |

| Late payment (tax liability unpaid) | BI rate + 5% p.a. (pro-rated daily) | KUP Law Art. 9(2a) |

| Combined late filing + late payment | Both penalties apply | Cumulative |

Long-Term Consequences:

| Source | URL |

|---|---|

| KUP Law Art. 3, 7, 9 (Filing and Payment Deadlines) | jdih.kemenkeu.go.id |

| PER-34/PJ/2017 (SPT Tahunan Procedures) | pajak.go.id |

| PMK-243/2014 (Fiscal Year Selection) | jdih.kemenkeu.go.id |

| DGT — SPT Tahunan Deadline Reference | pajak.go.id |

| Bank Indonesia — Current Benchmark Rate | bi.go.id |

Direct Answer: Indonesia's annual CIT filing requires a comprehensive documentation package that goes far beyond the SPT form itself. DGT has statutory authority to request any and all documents that support the figures reported in the SPT Tahunan — and failure to produce them during an audit carries severe penalties.

| Document Category | Specific Documents Required | Retention Period | Format |

|---|---|---|---|

| Financial Statements | • Audited balance sheet • Audited income statement • Cash flow statement • Notes to financials • Auditor's report with unqualified opinion (if audit required) |

10 years | PDF + XBRL (if threshold met) |

| Tax Ledger (Buku Besar Fiskal) | • General ledger with fiscal adjustments • Trial balance (commercial vs. fiscal) • Reconciliation of commercial to fiscal income |

10 years | Electronic + physical |

| Fixed Asset Register | • Detailed asset listing by class • Acquisition dates and costs • Depreciation method (commercial vs. tax) • Disposal records |

10 years | Electronic + physical |

| Inventory Records | • Year-end inventory count • Valuation method (FIFO, average, etc.) • Obsolescence provisions |

10 years | Electronic + physical |

| Related-Party Agreements | • Intercompany service agreements • Loan agreements (principal + interest terms) • Royalty/IP license agreements • Management fee agreements |

10 years | Physical signed originals |

| Transfer Pricing Documentation | • Master File (if part of MNE group) • Local File (functional analysis, benchmarking) • Declaration of TP Doc availability (Form attached to SPT) |

10 years | Electronic + physical |

| Tax Payment Evidence | • PPh 25 monthly payment receipts (all 12 months) • e-Billing confirmations • Bank debit advices |

10 years | Electronic |

| Withholding Tax Received | • Bukti Potong PPh 23 received from customers • Bukti Potong PPh 22 (import tax credits) • Foreign tax credit certificates (PPh 24) |

10 years | Physical + electronic |

| Tax Incentive Documentation | • Tax holiday approval letter (if applicable) • Tax allowance approval letter • Super deduction claim documentation |

10 years | Physical originals |

| Corporate Documents | • Articles of Association (latest version) • Shareholder register • RUPS minutes (if dividend distributed) • Director appointment deeds |

Permanent | Physical notarized originals |

Because most PT PMAs engage in cross-border related-party transactions, Transfer Pricing Documentation is almost always required. Under PMK-213/2016 and PER-22/PJ/2013, TP Doc must be available in Bahasa Indonesia and must be producible within one month of DGT's written request.

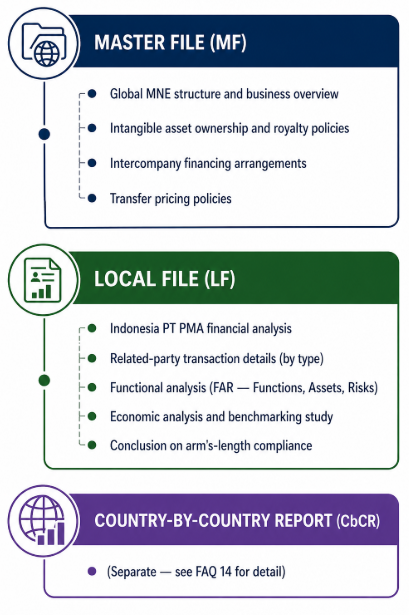

Master File Contents:

| Section | Required Information |

|---|---|

| Organizational Structure | • Global MNE chart • Ownership percentages • Geographic distribution |

| Business Description | • Nature of business by entity • Supply chain description • Key value drivers |

| Intangibles | • List of all IP owned by group • IP ownership by entity • R&D cost allocation • Royalty policies |

| Financing | • Intercompany financing arrangements • Central treasury function • Interest rate policies |

| Financial & Tax | • Consolidated group financials • List of APAs and rulings • List of all DTAs used |

Local File Contents:

| Section | Required Information |

|---|---|

| Company Overview | • Indonesia PT PMA description • Organizational chart • Management structure |

| Related-Party Transactions | • All transactions by type • Transaction amounts • Payment terms |

| Functional Analysis | • Functions performed • Assets employed • Risks assumed (FAR model) |

| Economic Analysis | • TP method selection (CUP, RPM, CPM, TNMM, PSM) • Benchmarking study • Comparable company analysis • Arm's-length range determination |

| Financial Data | • Segmented P&L for tested party • Financial ratios • 3-year trend analysis |

Filing Threshold: PT PMAs that are part of an MNE group with consolidated global revenue ≥ EUR 750 million (~IDR 12.75 trillion at 2026 exchange rates).

CbCR Table Structure (Three Tables Required):

Table 1: Financial & Employee Data by Jurisdiction

| Column | Data Point |

|---|---|

| Revenue | • Related-party revenue • Unrelated-party revenue • Total revenue |

| Profit/Loss | • Profit (loss) before tax |

| Tax | • Income tax paid (cash basis) • Income tax accrued (accrual basis) |

| Capital | • Stated capital |

| Earnings | • Accumulated earnings |

| Employees | • Number of employees (FTE) |

| Assets | • Tangible assets (excluding cash) |

Table 2: Entity Listing by Jurisdiction

| Column | Data Point |

|---|---|

| Entity name | Legal name of each constituent entity |

| Tax jurisdiction | Country of tax residence |

| Main business activity | From predefined list (Manufacturing, Sales, R&D, etc.) |

Table 3: Additional Information

Filing Deadline: 31 July (12 months after the fiscal year-end of the ultimate parent entity)

Legal Basis: KUP Law Article 28

All documents supporting the SPT Tahunan — and all underlying source documents (contracts, invoices, bank statements, emails evidencing business purpose) — must be retained for 10 years from the date the SPT is due.

Storage Format:

Audit Access: DGT has the right to request any or all documents at any time during the 10-year retention period. Taxpayers must produce requested documents within 14 days of written request (or longer period if formally agreed).

Penalty for Non-Production: Failure to produce documents during audit can result in:

| Source | URL |

|---|---|

| KUP Law Art. 28, 29 (Record-Keeping Obligations) | jdih.kemenkeu.go.id |

| PMK-213/2016 (Transfer Pricing Documentation) | jdih.kemenkeu.go.id |

| PER-22/PJ/2013 (TP Documentation Procedures) | pajak.go.id |

| PER-29/PJ/2017 (Country-by-Country Reporting) | pajak.go.id |

| PER-17/PJ/2015 (Bookkeeping Standards) | pajak.go.id |

| OECD — BEPS Action 13 Final Report | oecd.org/tax/beps |

| DGT — SPT Tahunan Supporting Documents Checklist | pajak.go.id |

Direct Answer: LKPM (annual investment reporting through OSS) and SPT Tahunan (annual tax return through CoreTax) are separate regulatory obligations to different authorities, but they are cross-validated by Indonesia's integrated government data systems. Discrepancies between LKPM-reported figures and tax-reported figures are a primary audit trigger for both BKPM compliance reviews and DGT tax audits.

| Dimension | LKPM (OSS/BKPM) | SPT Tahunan (CoreTax/DGT) |

|---|---|---|

| Governing Authority | Ministry of Investment (BKPM) | Directorate General of Taxes (DGT) |

| Legal Basis | Investment Law 25/2007; PP 5/2021 | Income Tax Law 36/2008; KUP Law 28/2007 |

| Primary Purpose | Monitor investment realization vs. plan | Calculate and collect corporate income tax |

| Filing Platform | OSS Portal (oss.go.id) | CoreTax (coretax.pajak.go.id) |

| Deadline (Calendar-Year) | End of February (following year) | 30 April (following year) |

| Reporting Frequency | Quarterly + Annual | Annual (with monthly installments PPh 25) |

| Key Metrics | Investment deployed, employment, production | Revenue, expenses, taxable income, tax liability |

| Cross-Check Fields | Revenue, employment, capital additions | Revenue, payroll, fixed assets |

| Penalty for Non-Filing | Investment status downgrade; license suspension risk | IDR 1,000,000 fine + interest on unpaid tax |

| Audit Consequence | BKPM operational compliance audit | DGT tax audit (full financial examination) |

Indonesia's National Single Window for Investment (NSWI) system now integrates data from OSS, CoreTax, Customs (INSW), BPJS, and Disnaker. Automated data-matching algorithms compare:

| Data Point | LKPM Field | SPT Tahunan Field | Acceptable Variance | Risk Level if Mismatched |

|---|---|---|---|---|

| Annual Revenue | "Realisasi Penjualan" | Form 1771-I: Total Revenue | ± 2% (rounding, timing) | HIGH — direct audit trigger |

| Fixed Asset Additions | "Realisasi Investasi: Peralatan" | Form 1771-II: Fixed Asset Additions | ± 5% (capitalization policy) | HIGH — TP audit risk |

| Employment Count | "Jumlah Tenaga Kerja Indonesia" | PPh 21 Annual Reconciliation (Form 1721-I) | ± 5 employees (turnover timing) | MEDIUM — Disnaker audit risk |

| Foreign Worker Count | "Jumlah Tenaga Kerja Asing" | PPh 26 Annual Summary | Zero tolerance | HIGH — immigration violation risk |

| Export Revenue | "Nilai Ekspor" | Revenue breakdown (if disclosed) | ± 3% (Incoterms, FX timing) | MEDIUM — customs cross-check |

Step-by-Step:

| Step | Action | Details |

|---|---|---|

| 1 | Login to OSS Portal | Access oss.go.id using the company’s OSS account (linked to NIB) |

| 2 | Navigate to LKPM Menu | Select "LKPM Tahunan" (Annual Report) |

| 3 | Select Reporting Period | Choose the relevant fiscal year being reported |

| Section | Category | Details |

|---|---|---|

| A | Investment Realization | Land acquisition cost (actual vs. plan) |

| Building construction cost (actual vs. plan) | ||

| Machinery & equipment (actual vs. plan) | ||

| Working capital deployed (actual vs. plan) | ||

| B | Employment | Indonesian workers (by education level) |

| Foreign workers (by nationality and position) | ||

| Total payroll expense (IDR) | ||

| C | Production / Operations | Revenue (sales, services) |

| Production output (units, if manufacturing) | ||

| Capacity utilization (%) | ||

| Export value (if applicable) | ||

| D | Compliance | Environmental permits (status) |

| Building permits (IMB status) | ||

| Operational licenses (status) | ||

| Tax filing confirmation (NPWP + SPT filing date) |

| Document Type | Details |

|---|---|

| Financial Statements | Audited balance sheet and profit & loss statement |

| SPT Tahunan Confirmation | Screenshot from CoreTax system |

| BPJS Summary | Annual contribution report |

| Export Documents | Export declaration summary (if applicable) |

| Step | Action | Details |

|---|---|---|

| 4 | Submit and Generate Receipt | Submit LKPM and download PDF receipt for records |

Post-Submission: BKPM's automated system compares submitted LKPM data against:

Red Flags for BKPM Review:

Scenario 1: Revenue Discrepancy

| Section | Details |

|---|---|

| Reported Figures | LKPM Annual Revenue: IDR 75,000,000,000 SPT Revenue (1771-I): IDR 68,000,000,000 Discrepancy: IDR 7,000,000,000 (9.3%) |

| Automated System Action | Flag sent to BKPM analyst Cross-reference flag sent to DGT Tax Office (KPP) Taxpayer account marked for "clarification required" |

| Possible Causes | LKPM includes non-operating income; SPT separates it Timing difference (revenue recognition method) LKPM in gross; SPT in net (after returns/allowances) Error in one or both filings |

| Taxpayer Action Required | Prepare written explanation (Klarifikasi) Attach reconciliation schedule Submit to both BKPM and DGT within 14 days of notice If error in SPT: file Pembetulan (correction) |

Scenario 2: Employment Count Discrepancy

| Category | Details |

|---|---|

| Reported Figures | LKPM Employment: 145 employees PPh 21 Annual Filing: 132 employees BPJS Registered: 138 employees |

| Discrepancy Identified | 3-way mismatch across reporting systems |

| Automated System Action | Flag to Disnaker (Labor Office) Cross-check against BPJS database Potential labor law violation review |

| Common Causes | Contractor/outsourced workers counted differently End-of-year hiring not yet processed in BPJS Resignations processed in tax but not yet in LKPM Deliberate underreporting to BPJS (compliance violation) |

| Resolution Steps | File corrected LKPM Register all employees in BPJS retroactively Pay retroactive contributions + administrative fine Update Wajib Lapor Ketenagakerjaan (Disnaker) |

Recommended Timeline:

| Date | Milestone | Key Actions |

|---|---|---|

| 15 January 2026 | Year-End Close | Finalize year-end GL; extract revenue, fixed assets, payroll data |

| 31 January 2026 | Audit Completion | Complete audit; obtain audited financials |

| 10 February 2026 | Draft Preparation | Prepare DRAFT LKPM using audited data; prepare DRAFT SPT Tahunan fiscal reconciliation |

| 15 February 2026 | Reconciliation Checkpoint | Compare LKPM revenue vs. SPT revenue; compare LKPM employment vs. PPh 21 headcount; compare LKPM capex vs. fixed asset additions (SPT 1771-II); document and resolve all variances > 2% |

| 28 February 2026 | LKPM Filing Deadline | File LKPM via OSS |

| 30 March 2026 | SPT Finalization | Finalize SPT Tahunan (incorporating any LKPM adjustments) |

| 31 May 2026 | SPT Filing Deadline | File SPT Tahunan via CoreTax |

| Source | URL |

|---|---|

| Investment Law (UU 25/2007) | jdih.setneg.go.id |

| PP 5/2021 (Investment Facilitation Risk-Based Approach) | jdih.setneg.go.id |

| OSS Portal — LKPM Submission | oss.go.id |

| Ministry of Investment — LKPM Guidelines | investindonesia.go.id |

| DGT — CoreTax Filing Portal | coretax.pajak.go.id |

| National Single Window for Investment (NSWI) | nswi.go.id |